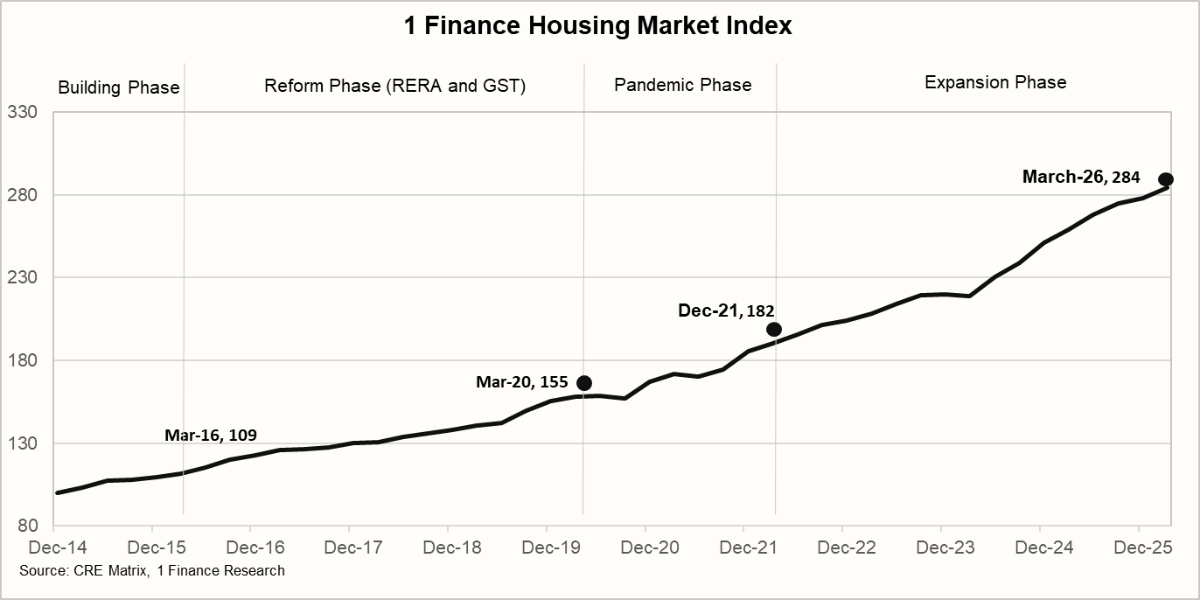

India's housing market just posted its most revealing quarter in years, and the message is uncomfortable for developers still running the old playbook. Launches are climbing in nearly every major market, but sales are falling behind everywhere outside Maharashtra. The 1 Finance Housing Market Index, built on RERA-registered transaction data, has compounded at 10.6% over five years to reach 284 in March 2026. That headline masks the regime shift underneath: inventory discipline, execution track records, and product sizing are now separating the markets that compound from the ones that stay range-bound.

We see Q1 2026 as the quarter where three forces collided. First, RERA slippages are no longer a background irritant; they are actively repricing entire cities. Second, buyers have stopped paying a premium for smaller flats, forcing developers to rethink unit sizing for the first time in a decade. Third, the overhang of older unsold stock is dragging both primary and secondary returns in Mumbai and Thane to levels that make residential look like a fixed deposit.

| Key Takeaways |

|---|

|

|

|

|

|

The 1 Finance Housing Market Index Shows a Regime Shift

The 1 Finance Housing Market Index captures the long upcycle, but also hints at the current regime shift. Based on RERA-registered transaction data, the index delivered a 10.6% CAGR over five years, reaching 284 in March 2026.

While earlier growth was driven by strong end-user momentum, the current phase is more measured, with inventory discipline shaping outcomes across cities.

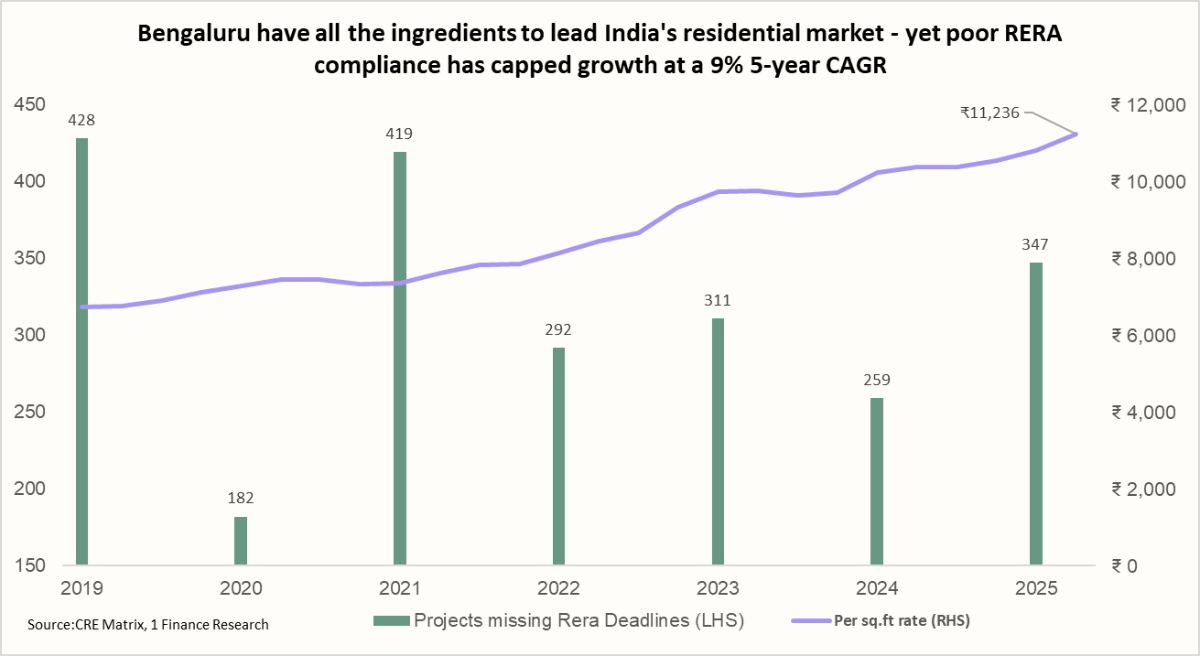

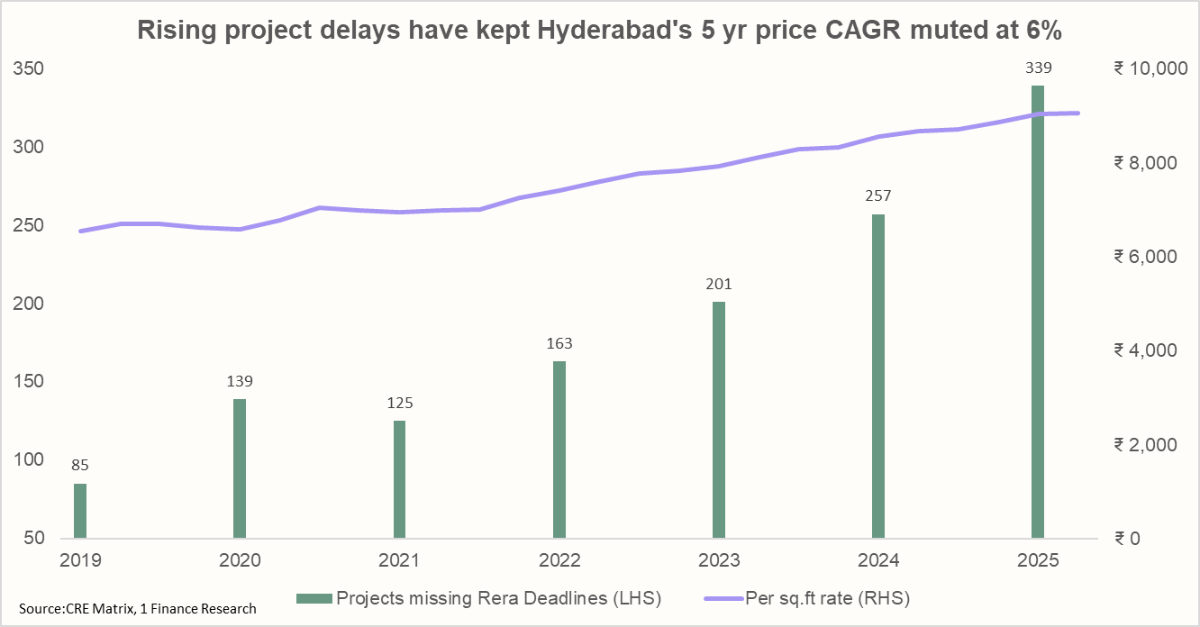

Bengaluru and Hyderabad Are Drowning in Their Own Supply

Bengaluru launched 26,297 units in Q1 2026, an all-time high, and sold only 16,745. Unsold inventory has climbed to 87,796 units, a 20-quarter peak. We count 214 projects in the city that missed RERA-mandated completion timelines this quarter alone, and buyer confidence in fresh launches is taking a visible hit on pricing. The macromarket split is widening: Bengaluru Southwest rose 6% QoQ and 25% YoY, while Bengaluru Central has slid 24% over the past year. Bengaluru Northwest led the quarter at 25% growth. The Bengaluru Housing Market Index has compounded at 11% annually over five years, respectable on paper, but arguably understating the tailwind the tech sector has provided.

Hyderabad is worse. Sales fell to 11,342 units, the weakest quarter in 21 quarters, while unsold stock hit a record 1,28,869 units. Launches have continued at pace regardless, and 299 projects missed RERA timelines this quarter. The IT corridor of Hyderabad Southwest remains the lone consistent performer at 2% QoQ and 11% YoY price growth, while the Northwest, Northeast, and Southeast micromarkets have struggled. The Hyderabad Housing Market Index has compounded at 9% over five years, a figure that understates the long-term tailwind from IT and pharma but increasingly reflects developers' inability to match supply to demand.

The pattern is the same in both cities: launches outpacing absorption, RERA slippages mounting, and unsold stock accumulating. Until launches slow or execution improves, neither market will sustain pricing power. We expect both to remain range-bound through the rest of 2026.

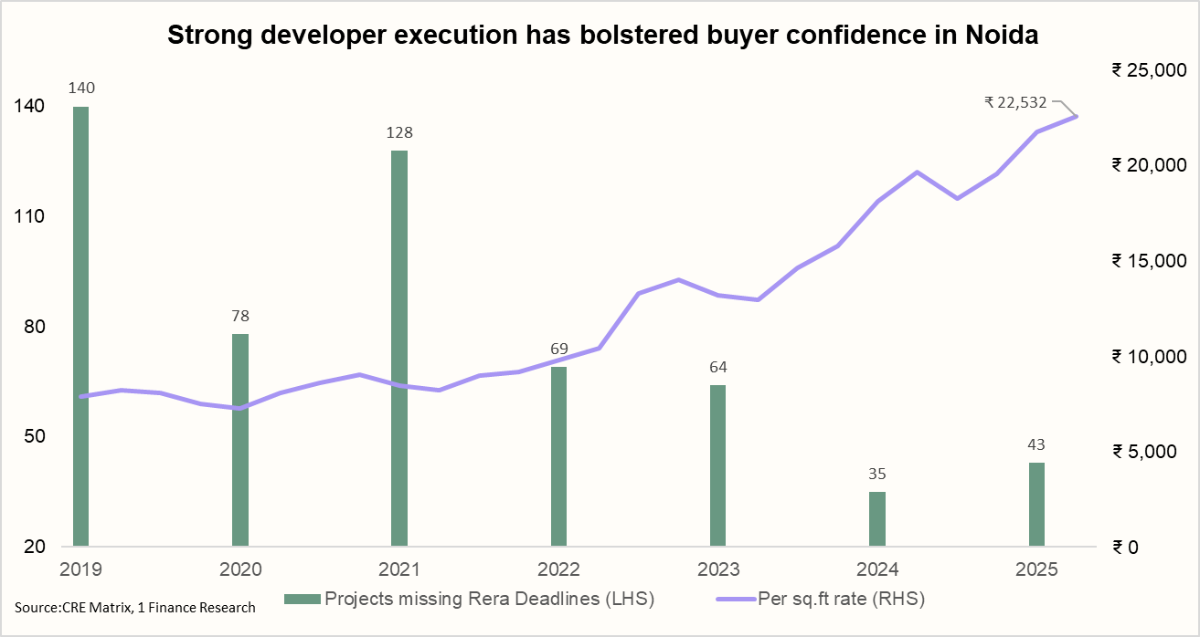

Noida Has Earned Its Premium Over Gurugram

The 1 Finance Delhi NCR Housing Market Index has compounded at 14% over five years, but the internal divergence is dramatic. Noida's PSF has now overtaken Gurugram's at ₹22,532 vs ₹19,351 as of March 2026, a reversal that would have been unthinkable a few years ago.

Noida's 23% five-year CAGR, the highest in India, is built on a dramatic improvement in execution. The number of delayed projects in Noida has fallen 70% since 2019. Buyers have rewarded that turnaround with sustained demand and pricing power.

Gurugram, meanwhile, has corrected nearly 20%. Persistent civic issues (drainage, traffic, waste management) have eroded the premium positioning that once justified higher PSF pricing. Faridabad led the NCR quarter at 90% growth, suggesting capital is migrating toward markets where infrastructure delivery is tangible.

The Delhi NCR story is the clearest proof point in the data for something we have been arguing for several quarters: civic infrastructure is now a pricing input, not a background detail. Developers who build in corridors with functioning roads, drainage, and services will compound. The rest will keep losing ground regardless of how premium the address used to be.

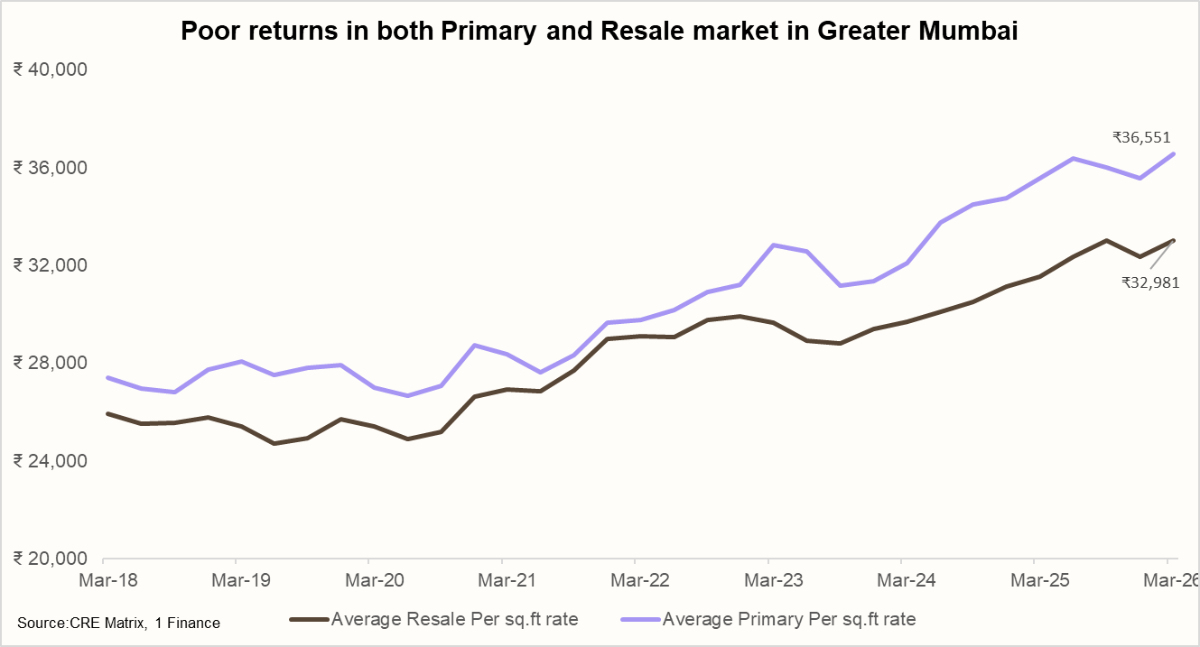

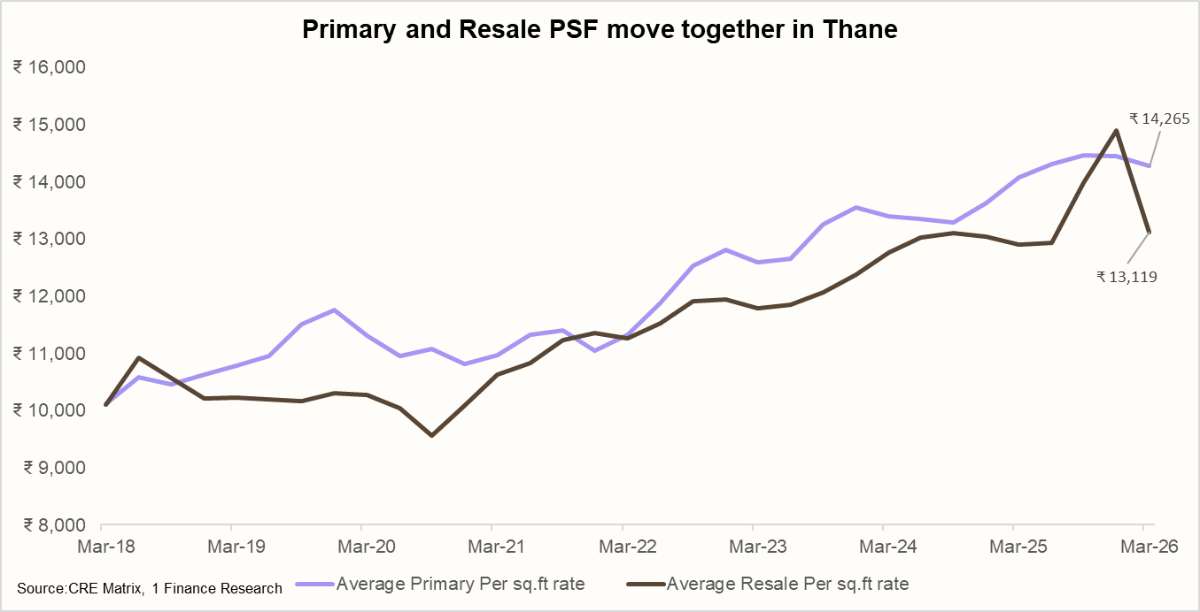

Mumbai and Thane Are Trapped by Their Own Backlog

Greater Mumbai posted its busiest quarter in years with 16,653 launches (a 15-quarter high) and 13,171 sales (a 17-quarter high). On the surface, that looks like a market firing on all cylinders. Look underneath, and the picture is different.

Newly launched inventory cleared at ₹35,180 PSF, a 25% discount to the ₹47,095 PSF for Q4 2025 launches. The five-year picture tells the same story: primary and secondary have returned a muted 4% and 5% annualised, respectively.

The culprit is a large overhang of old unsold stock. In the last 12 months, 38% of units sold in Greater Mumbai were older than three years, transacting at ₹28,650 PSF, a 15% discount to the latest resale PSF, with carpet areas 22% larger. This older stock is cheaper and roomier, which lets it undercut resale units on both price and size. That drags secondary returns down while simultaneously forcing developers to discount new launches heavily to compete, capping primary returns too.

Thane mirrors this dynamic almost exactly. Primary and secondary have returned 5% and 4% annualised over five years. 38% of units sold in the last 12 months were over three years old, transacting at ₹12,010 PSF at an 8% discount to the latest secondary PSF, with only marginally smaller carpet areas. Navi Mumbai was the most consistent performer in the cluster at 5% QoQ and 7% YoY growth, backed by tangible infrastructure delivery.

For advisors with clients holding Mumbai or Thane residential as an investment, the math is clear: until this old inventory clears, returns will struggle to break out of the 4-5% annualised band. That puts residential in these markets firmly behind even short-duration debt on a risk-adjusted basis.

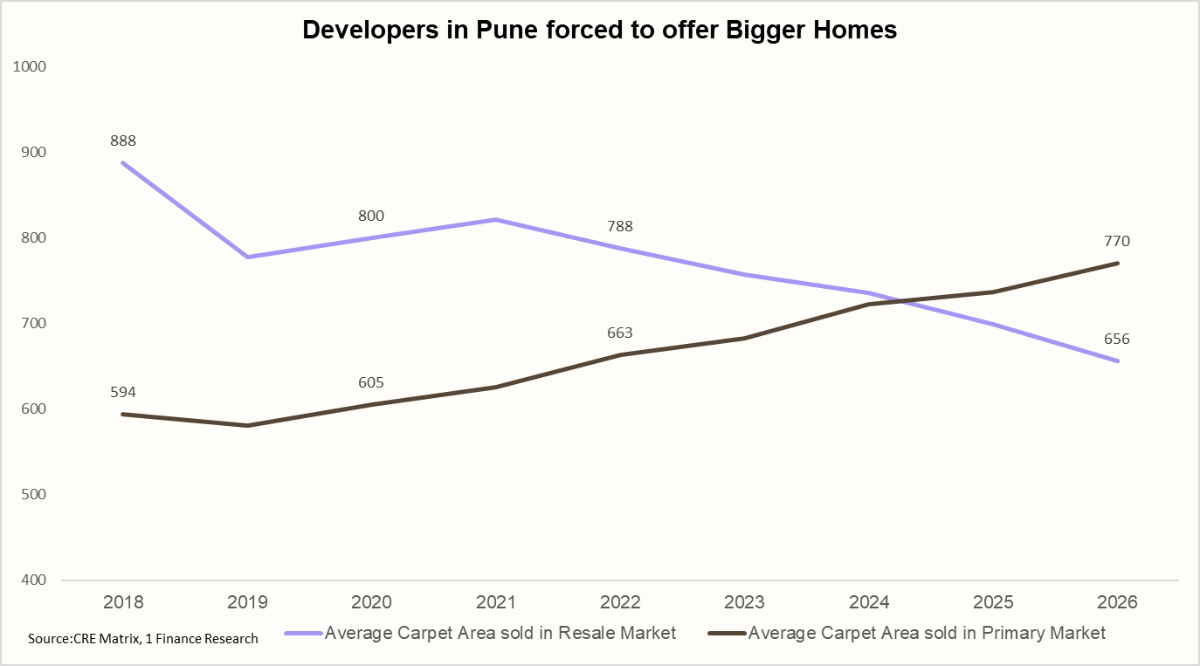

Pune Shows What Happens When Developers Listen to Buyers

Pune is the standout story in Maharashtra and arguably the cleanest housing market in the country right now. Unsold inventory fell to 2,83,920 units, its lowest in 12 quarters, as sales outpaced launches.

But the more interesting shift is in the convergence of pricing and sizing. In 2020, new flats in Pune sold at a 12% PSF premium over older resale stock. Today, that premium has all but disappeared at just 0.7% (₹11,690 vs ₹11,610). The reason is space. Buyers have consistently paid up for larger units, and older resale flats were bigger. Resale returns have beaten primary in four of the last six years precisely because of this sizing advantage.

Developers have now responded. In 2025, for the first time in over a decade, the average primary flat sold was bigger than the average resale flat, and the gap widened in Q1 2026 to 770 sq ft for primary vs 656 sq ft for resale. Since 2020, primary PSF has returned only 5% annualised, but the primary area sold has grown 27%.

Pune is showing the rest of the market what the new equilibrium looks like: the days of charging more per square foot without offering more space are numbered. Developers who keep shrinking unit sizes will watch resale stock eat their lunch.

Outlook

The Q1 2026 picture points to a few patterns worth carrying into the rest of the year. Execution will increasingly separate winners from losers - Noida's rise has shown that buyers reward developers who deliver on time, and markets where RERA slippages are mounting will find it harder to sustain pricing. Civic infrastructure is now a pricing input, not a background detail; cities and corridors that fail on drainage, traffic, and basic services will keep losing ground regardless of how premium their address used to be. On product, the days of charging more per square foot without offering more space look numbered - Pune has already shown that when developers stop expanding sizes, resale stock eats their lunch. Supply discipline will matter more than ever: markets that keep launching faster than they sell will stay range-bound until inventory clears, while disciplined markets will see pricing power return first.

We expect execution and inventory discipline to be the dominant themes through 2026. The markets that launch responsibly and deliver on time will see pricing power return first. The rest will keep waiting.