India's private sector just did something it hasn't in years: it opened its wallet. Private capital expenditure jumped 67% year-on-year to ₹7.7 lakh crore in the first half of FY26, per CII, up from ₹4.6 lakh crore a year earlier. After years of hearing about a "private capex crisis", this looks like the turnaround everyone's been waiting for.

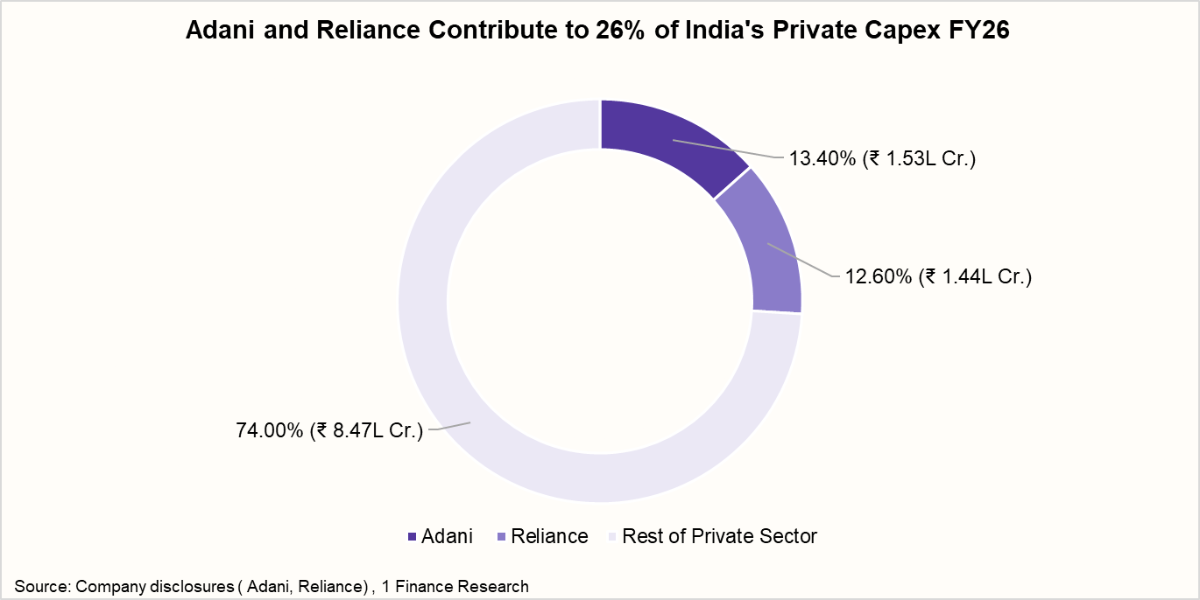

But look at the full-year picture, and the story gets more concentrated. Adani and Reliance alone spent a combined ₹3.2 lakh crore in FY26, roughly 28% of the National Statistical Office's estimated total private capex for the year. Is India Inc. genuinely investing again, or are two conglomerates carrying much of the story alone?

What Is Capex and Why Does It Matter

Capex, or capital expenditure, is money a business spends on long-term assets such as factories, machinery, and technology, rather than day-to-day costs like salaries or raw materials. Think of it as the difference between buying a new production line and paying this month's electricity bill.

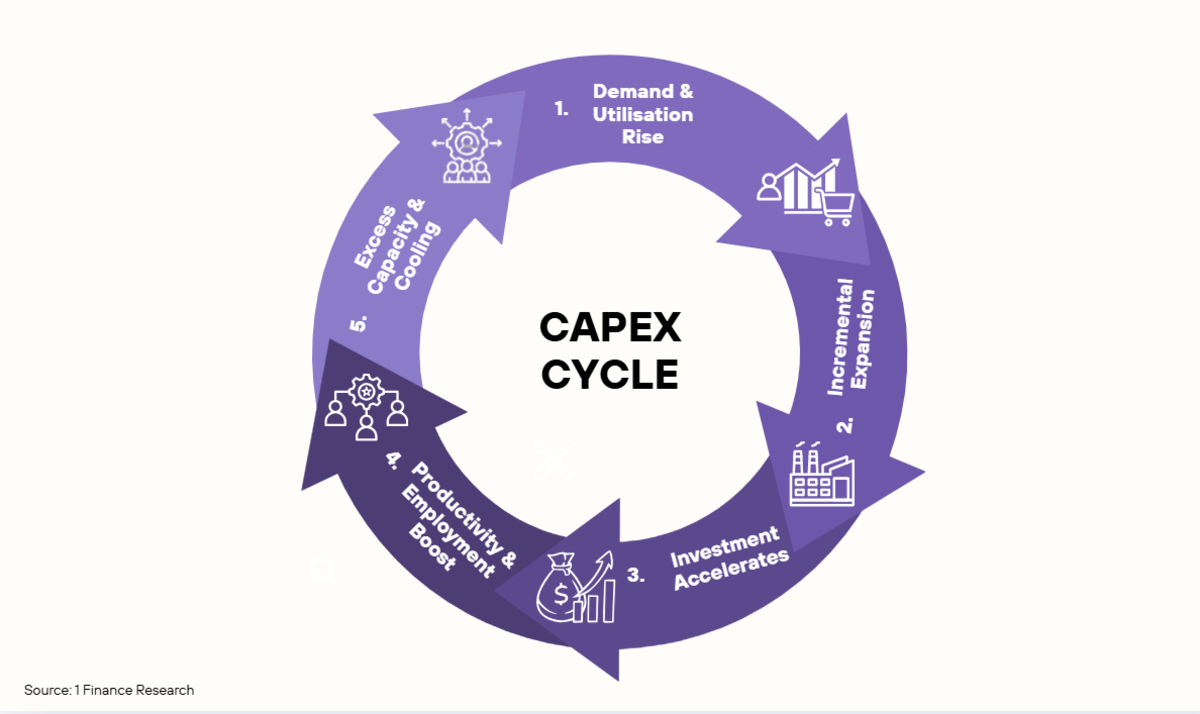

Capex tends to move in a predictable cycle:

- Demand improves, and capacity utilisation begins to rise

- Firms respond with incremental expansion to keep pace

- Investment accelerates once utilisation crosses a comfortable threshold

- Productivity and employment improve as new capacity comes online

- Excess capacity eventually builds, and the cycle cools until demand catches up again

This distinction matters because consumption drives growth in the present, while capex determines what an economy can produce in the future. Sustained investment raises potential GDP, strengthens export competitiveness, and eases the supply-side constraints that often fuel inflation.

Public Capex vs Private Capex

Not all capital expenditure comes from the same source, and the distinction shapes how each is read as an economic signal.

| How Public Capex Differs from Private Capex | ||

|---|---|---|

| Aspect | Public Capex | Private Capex |

| Funded by | Budgetary allocations, government borrowing, PSU spending | Company earnings, private borrowing, and equity capital |

| Primary objective | Long-term capacity building, not profitability | Profitability and return on investment |

| Key driver | Policy priorities and fiscal strategy | Demand visibility, cost of capital, and business confidence |

| Typical spend | Roads, railways, ports, and power infrastructure | Factories, machinery, technology, and expansion projects |

| What it signals | Government's growth priorities | Genuine market confidence in future demand |

| Can it be mandated? | Yes, decided through budget allocation | No, depends entirely on business decision-making |

This is why economists track private capex so closely. Public capex can be switched on by a budget decision. Private capex cannot be mandated; it only happens when businesses genuinely believe the future is worth betting on.

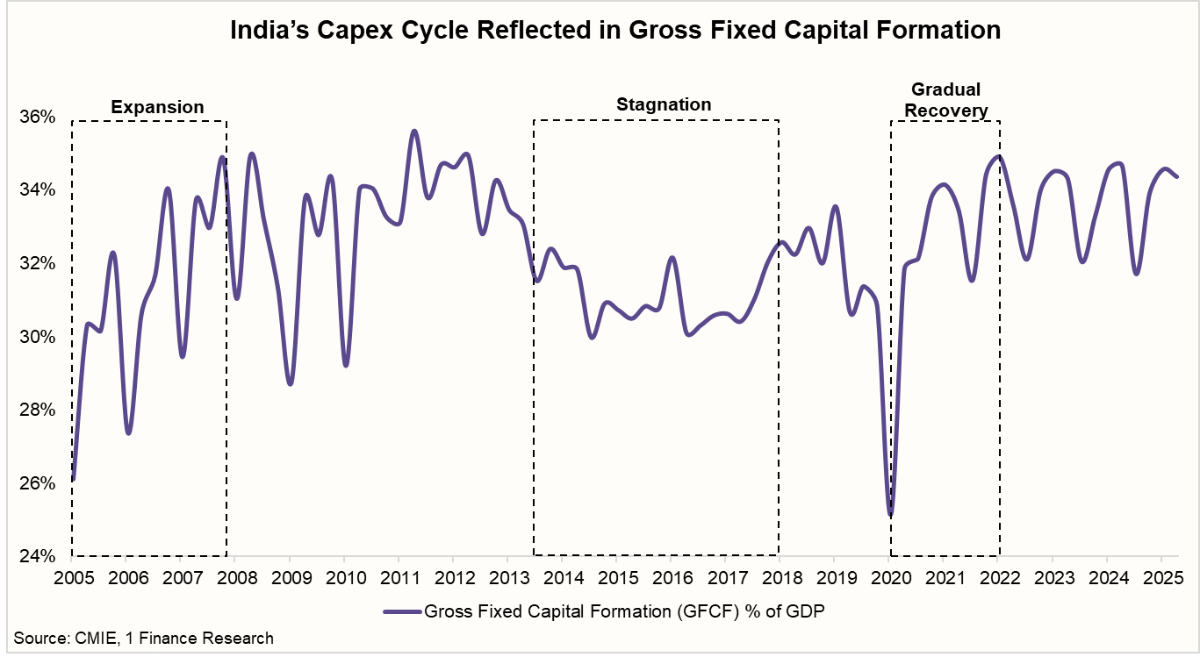

India's Capex Journey Over the Last Two Decades

India’s investment story over the last twenty years can broadly be understood in three phases: expansion, stagnation, and gradual recovery.

The years leading up to the Global Financial Crisis saw a powerful private investment boom. Corporate confidence was high, global demand was strong, and domestic reforms supported capital formation. Gross Fixed Capital Formation (GFCF) as a share of GDP reached elevated levels, driven largely by private firms expanding capacity across infrastructure, manufacturing, and services.

That momentum did not survive the post-crisis decade. The 2010s were marked by stressed corporate balance sheets and rising non-performing assets in the banking system. The so-called “twin balance sheet problem” curtailed risk-taking, and private capex slowed sharply. Investment rates declined steadily, even as consumption and services kept headline growth afloat.

The pandemic delivered a further shock, pushing investment activity to cyclical lows. It was only after FY 2021–22 that a recovery began, driven not by private firms but by an aggressive and sustained increase in government capital expenditure.

How Government Capex Drove India’s Growth

Recognising the private sector’s prolonged hesitation, the government made capital expenditure the centrepiece of its own growth strategy. Since FY18, successive budgets have prioritised capital spending over revenue spending, a deliberate anchor for growth, not a reactive move.

The money flowed into roads, railways, ports, power transmission, defence, urban infrastructure, and digital networks. Flagship programmes like Gati Shakti and the National Infrastructure Pipeline cut execution delays and logistics costs, the very bottlenecks that once discouraged private investment.

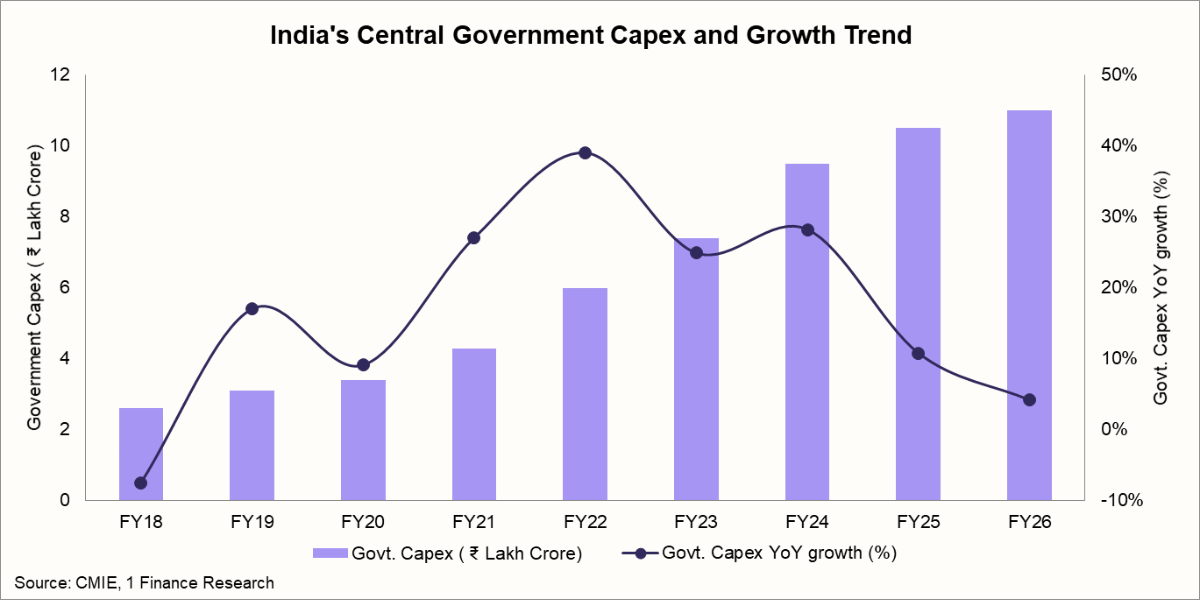

The scale has been striking. Central government capex has climbed from ₹2.63 lakh crore in FY18 to nearly ₹11 lakh crore in FY26, more than a four-fold increase in under a decade. Govt. Capex growth peaked at 39% in FY22, before moderating to single digits by FY26 as the base got larger. Even as the pace of growth has slowed, the scale of commitment keeps rising year after year.

Public capex stabilised the economy. The real question: has it drawn private capital back, or is the gap here to stay?

Is Private Capex Reviving in India

For years, India's private sector held back. Now the numbers suggest something has shifted, though not evenly.

The headline number

According to the Confederation of Indian Industry (CII), private capital expenditure jumped 67% to ₹7.7 lakh crore in the first half of FY26, up from ₹4.6 lakh crore a year earlier. CII has called it the strongest investment signal in over a decade. After years of hearing about a "private capex crisis," this is the number everyone's been waiting for.

Where the money is going

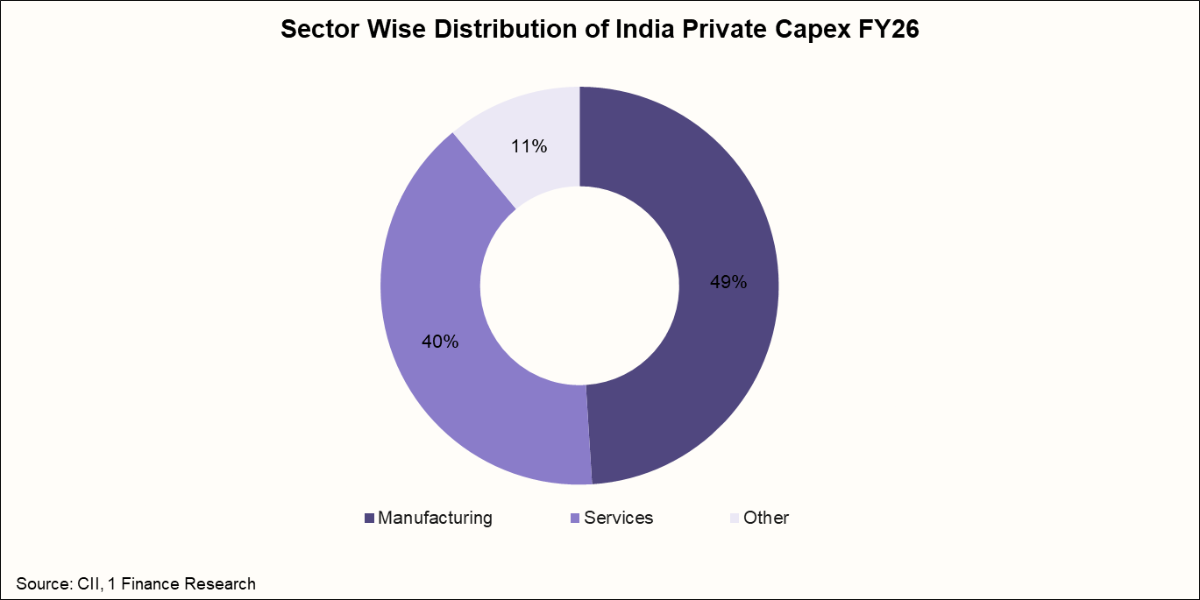

The spread across sectors tells its own story:

- Manufacturing: around ₹3.8 lakh crore, roughly half the total, led by metals, automobiles, and chemicals

- Services: around ₹3.1 lakh crore, driven by trading, communications, and IT/ITeS

- New-age momentum: data centres, renewables, and electronics (PLI-linked) are where growth is accelerating fastest, even if legacy manufacturing still holds the larger absolute share

The supporting evidence

This isn't a one-off number. Several indicators point in the same direction:

- Capacity utilisation climbed from 74.3% in Q2 FY26 to 75.6% in Q3 FY26

- Order books have shown double-digit growth through FY26

- Bank credit growth accelerated from around 10% in H1 FY26 to nearly 14% in H2 FY26

- Corporate balance sheets are healthier, with lower leverage and stronger cash flows

- The cost of capital has fallen, making expansion cheaper to finance

The twist?

Zoom out to the full financial year, and the revival narrows fast. Adani and Reliance together accounted for a combined ₹2.97 lakh crore in FY26 capex, roughly 26% of the National Statistical Office's estimated total private capex for the year. Adani's own capex more than doubled in two years, from ₹70,000 crore to ₹1.53 lakh crore, its highest-ever annual capex by any Indian corporate. Much of this money is chasing the same global theme: AI infrastructure. Reliance has committed $110 billion to AI and data centres over the next seven years; Adani has pledged $100 billion by 2035 to build AI-enabled data centres, expanding AdaniConnex's national capacity from 2GW to a 5GW target.

The supporting evidence

This isn't a one-off number. Several indicators point in the same direction:

- Capacity utilisation climbed from 74.3% in Q2 FY26 to 75.6% in Q3 FY26

- Order books have shown double-digit growth through FY26

- Bank credit growth accelerated from around 10% in H1 FY26 to nearly 14% in H2 FY26

- Corporate balance sheets are healthier, with lower leverage and stronger cash flows

- The cost of capital has fallen, making expansion cheaper to finance

The twist?

Zoom out to the full financial year, and the revival narrows fast. Adani and Reliance together accounted for a combined ₹2.97 lakh crore in FY26 capex, roughly 26% of the National Statistical Office's estimated total private capex for the year. Adani's own capex more than doubled in two years, from ₹70,000 crore to ₹1.53 lakh crore, its highest-ever annual capex by any Indian corporate. Much of this money is chasing the same global theme: AI infrastructure. Reliance has committed $110 billion to AI and data centres over the next seven years; Adani has pledged $100 billion by 2035 to build AI-enabled data centres, expanding AdaniConnex's national capacity from 2GW to a 5GW target.

That kind of concentrated, deep-pocketed confidence is very different from thousands of mid-sized firms independently deciding to bet on India's future. And that difference shows up clearly outside these two conglomerates: the rest of private investment remains noticeably patchier. In one recent quarter, announced manufacturing investment value actually dipped roughly 3%, and the number of new projects fell over 10%, as traditional sectors like steel, cement, and autos stayed cautious rather than following the AI-infrastructure rush.

The real question

The data proves private capex is moving again. What it can't yet prove is whether India Inc., as a whole, has rediscovered its risk appetite, or whether a handful of deep-pocketed conglomerates are simply making the biggest bets they can afford, while everyone else keeps watching.

Are animal spirits back in the economy?

Here's a puzzle the data alone can't solve. Balance sheets are healthier. Capital is cheaper. Bank credit is flowing. By classical economic logic, that should trigger a broad, economy-wide investment wave. It hasn't.

Keynes coined the term "animal spirits" to describe this gap, the idea that investment isn't purely mathematical, but driven by belief. Economists Akerlof and Shiller later broke the concept into five distinct forces: confidence, fairness, corruption, money illusion, and stories, the narratives people build the future around.

India's private capex revival looks like a story built almost entirely on two of these five: confidence and stories, not the other three.

- Confidence is narrow, not broad. It exists strongly among a handful of large, deep-pocketed conglomerates with long investment horizons, but hasn't spread to mid-sized firms still exposed to uneven domestic demand.

- Stories are doing heavy lifting. The dominant narrative driving the biggest checks right now is global AI infrastructure. Reliance's $110 billion AI and data centre commitment, Adani's 3GW data centre platform. This is a narrative-led investment wave as much as a demand-led one.

- Fairness, corruption, and money illusion are largely inactive here; this isn't a story about wage disputes, institutional trust, or inflation confusion. It's specifically a confidence-and-narrative story.

That distinction matters. Narrative-driven, concentrated confidence is real, but it's also more fragile than broad-based confidence built on demand across thousands of firms. A shift in the AI narrative, or a stumble at one large conglomerate, could shake the "story" holding this revival together far more easily than it could shake a genuinely diversified boom.

India’s Capex Growth Compared to Other Countries

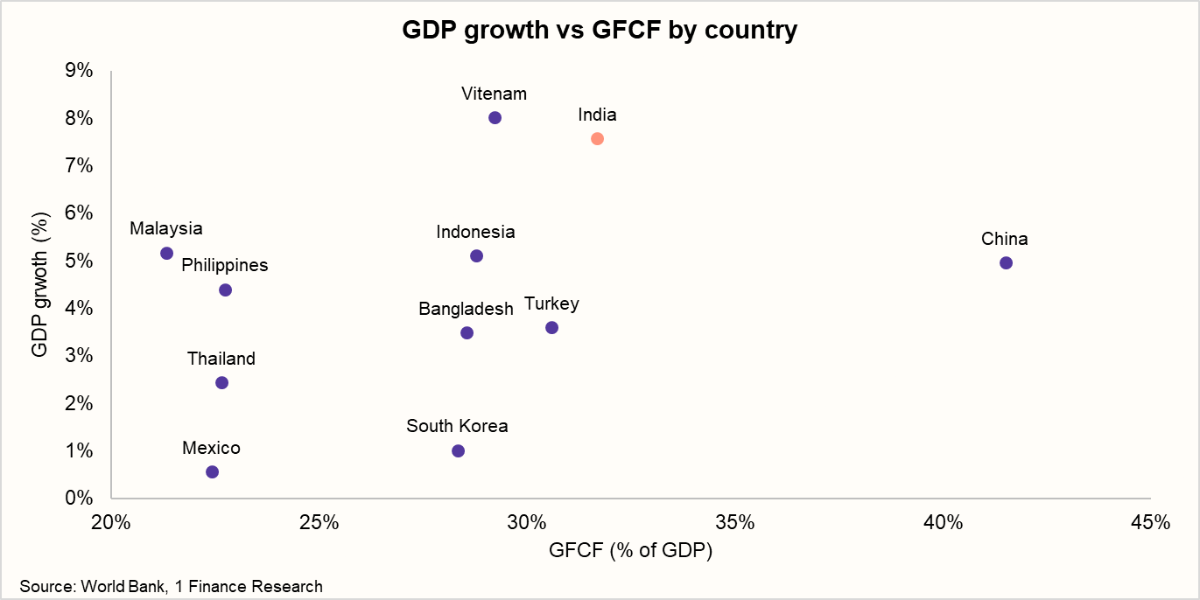

Placed next to its peers, India's investment story looks solid, but the more interesting story is what it's getting in return.

On investment intensity alone, India sits mid-pack, well behind China's investment-heavy model, but ahead of most Southeast Asian and Latin American peers. The real story is growth per rupee invested: India's 7.57% GDP growth is the second-highest in this group, trailing only Vietnam (8.02%), despite investing a similar share of GDP. China, by contrast, invests far more (41.5% of GDP) but grew less than a third as fast.

The one country worth watching closely is Vietnam; it now matches India on investment intensity and slightly beats it on growth, making it India's closest competitor in the "efficient investor" category, not the usual suspects like China.

Risks to India’s Private Capex Revival

Even the most convincing revival has an asterisk.

- Geopolitical risk: This tops the list. CareEdge and Crisil warn that a prolonged West Asia conflict or crude above $100/barrel could raise imported inflation, limit the RBI's room to keep rates low, and squeeze borrowing costs, hitting MSMEs and energy-intensive sectors hardest.

- Uneven consumption: This is the quieter risk. Thermax and Siemens have both flagged a "wait and see" stance on new capacity, since many firms can still meet demand by running existing plants harder, not building new ones.

- Global trade uncertainty: Tariffs, an unpredictable Fed, and mixed signals from China add further caution, as JSW Steel's own earnings commentary reflects.

- Concentration is itself a risk: If two or three groups carry the private capex number, a shock to any one of them could swing the entire figure.

India’s Private Capex Revival Outlook

India's private capex story is, at last, a genuinely good headline. The CII's 67% jump, healthier balance sheets, cheaper capital, and rising bank credit are all real, verifiable signs that the decade-long hesitation is finally breaking.

But the full picture is more nuanced than the headline. Much of the heavy lifting is still being done by two conglomerates, i.e. Adani group & Reliance, betting on a single global theme, AI infrastructure, rather than a broad base of Indian businesses independently backing India's own demand story. Balance sheets have healed faster than confidence has.

Placed against its peers, India isn't the region's biggest investor, but it is, for now, one of its most efficient, translating a moderate investment ratio into among the strongest growth rates in its competitive set.

Whether 2026 becomes the year confidence finally broadens beyond Adani and Reliance, beyond AI, into the thousands of mid-sized firms still watching from the sidelines, remains the real test ahead.

What This Means for Investors and Advisors

For investors, the capex story isn't just macro trivia; it's a map of where earnings growth is likely to concentrate next.

The clearest beneficiaries sit in capital goods, defence manufacturing, and electronics manufacturing services (EMS) sectors directly tied to both government infrastructure spending and the new private capex wave. Companies with exposure to AI infrastructure, data centres, and power transmission are positioned closest to where Adani and Reliance are deploying capital. Select real estate and construction-linked names may also benefit as execution catches up with announcements.

The caution flag from this piece applies here too: much of the visible momentum is concentrated in a handful of large, promoter-driven groups. Advisors should weigh broad "capex theme" exposure against the risk of unintentionally overweighting two or three conglomerates through multiple holdings.

As with any thematic view, timing and stock selection matter more than the macro story alone.