If you've taken a loan against your shares or traded on margin anytime in the last two years, you've been part of a boom that's caught the Reserve Bank of India's attention, and it hasn't slowed down yet. India's margin trading facility (MTF) book, where money brokers lend investors to buy shares with leverage, has grown from around ₹25,000 crore in FY23 to a record ₹1.4 lakh crore in June 2026, marking three straight months of growth even after a brief dip earlier in the year. The National Stock Exchange alone accounts for 96% of this activity. That's a lot of borrowed money chasing stock market returns, right as new rules are about to bite.

In February 2026, the RBI rolled out a fresh set of regulations tightening the way banks fund loans against securities (LAS) and back brokers' margin trading books, with compliance kicking in from July 1, 2026. In other words, market leverage just hit a new high at almost the exact moment regulators are moving to rein it in. Whether you're an investor using LAS for personal needs, a trader on margin, or an advisor guiding clients through this shift, here's everything you need to know about what's changed, why it matters, and what to expect next.

What Is a Loan Against Securities (LAS)?

A Loan Against Securities (LAS) lets you pledge shares, mutual funds, or bonds as collateral to get a loan, without selling them. Think of it as a loan against your portfolio instead of your property.

Why investors use it: to raise quick cash for personal or business needs without triggering capital gains tax or losing future upside on their holdings. It's typically faster and cheaper than an unsecured personal loan since the lender already holds collateral.

How it works: the lender values your pledged securities and offers a loan, commonly around 50% of their market value. Your shares stay in your demat account (still earning dividends) but get marked as pledged until the loan is repaid. If share prices fall sharply, you may get a margin call, requiring extra collateral or partial repayment.

What Changed in RBI’s LAS Rules 2026

RBI's February 2026 amendments target two specific gaps in how loans against securities were being used. Here's what's actually new:

- End-use restriction: LAS funds can no longer be used to buy shares, apply for IPOs, or fund margin trading. Previously, some borrowers used LAS as a backdoor way to add fresh leverage to their market exposure, pledge existing shares, borrow against them, and pump that money right back into the market. RBI has now closed this loop: the loan has to go toward its stated personal or business purpose, not more market speculation.

- A system-wide borrowing cap: This is the bigger structural change. Individuals can now borrow up to ₹1 crore against shares, REITs, and InvITs, but critically, this cap applies across the entire banking system, not per bank. Previously, a borrower could pledge the same portfolio (or different slices of it) with multiple banks and quietly build up exposure far beyond what any single lender could see. Now, lenders are expected to check total exposure across the system before sanctioning a loan.

- A separate, tighter cap for IPO and ESOP funding: Loans specifically taken to subscribe to IPO shares or exercise ESOPs are capped at ₹25 lakh per person, again aggregated across all banks combined. This is meaningfully lower than the general LAS cap, reflecting RBI's specific concern about leveraged bets on new listings.

| LAS Rules Before and After 2026 | ||

|---|---|---|

| Rule Parameter | Old rules | New rules |

| End - use | Loans allowed for personal/business needs, subscribing to IPOs, and buying shares in the secondary market | Cannot be used for buying shares, IPOs, or margin trading |

| Borrowing cap | ₹20 lakh per individual for demat shares, ₹10 lakh for physical shares | ₹1 crore per person, system-wide |

| IPO/ESOP funding cap | ₹10 lakh per individual | ₹25 lakh per person, system-wide |

Taken together, these changes make LAS a genuinely restricted personal/business liquidity tool again, not a quiet side-door into leveraged market exposure. For most ordinary investors borrowing well under ₹1 crore for legitimate needs, nothing changes day to day. The real impact falls on HNIs and larger borrowers who were stacking exposure across multiple lenders.

What Changed for Broker MTF Funding

While the LAS rules target individual borrowers, RBI's second set of changes hits the supply side of the leverage chain, the banks that fund brokers, who in turn offer a Margin Trading Facility (MTF) to retail investors.

- Higher cash collateral requirement: Banks funding brokers' MTF books must now ensure at least 50% of the collateral is cash or cash equivalents, rather than relying heavily on pledged securities. This makes broker funding meaningfully more expensive and less flexible than before.

- Bigger haircuts on share collateral: When brokers pledge equity shares as collateral for bank funding, banks must now apply a minimum 40% haircut, meaning ₹100 worth of pledged shares only counts as ₹60 in usable lending value. This directly shrinks how much brokers can borrow against the same pool of shares.

- Restriction on proprietary trading funding: Banks generally cannot fund brokers to buy securities for their own account (proprietary trading), closing off another channel where bank money was indirectly fueling market exposure. Some limited exceptions exist for market-making activity, provided the funding is fully backed by cash or cash equivalents.

| Margin Trading Funding Rules Before and After 2026 | ||

|---|---|---|

| Rule Parameter | Old rules | New rules |

| Cash collateral requirement | No fixed minimum | At least 50% cash or cash equivalents |

| Haircut on pledged shares | Lender discretion, often lower | Minimum 40% haircut mandated |

| Funding for proprietary trading | Generally allowed | Restricted, limited exceptions only |

Why this matters: brokers who lean heavily on bank credit to fund their MTF books, rather than using their own capital, now face a genuinely higher cost of doing business. That cost tends to get passed on to retail investors in the form of higher MTF interest rates or tighter eligibility on which stocks qualify for margin funding.

When Do the RBI New Rules Take Effect

Regulations rarely land exactly as first announced, and this one is a good example of how that plays out in practice. What started as a tight, seven-week compliance window for banks and brokers ended up stretched into a longer, negotiated rollout, and that timeline shift is part of why market activity kept climbing through mid-2026 even as the rules loomed.

- The original timeline: RBI announced the new LAS and MTF funding rules on February 13, 2026, with an initial compliance deadline of April 1, 2026, giving banks and brokers just under seven weeks to fall in line.

- The pushback: That timeline turned out to be tight. Banks and brokers flagged that reworking funding structures, collateral systems, and internal risk models on such short notice risked disrupting normal lending operations rather than just curbing speculative excess. Industry bodies pushed RBI for more runway to implement the changes properly.

- The extension: RBI responded by deferring the deadline to July 1, 2026, a three-month extension that gave the industry more breathing room while keeping the substance of the rules unchanged.

Why this matters for your understanding of the story: This kind of extension is fairly normal in Indian financial regulation; the RBI has a track record of allowing implementation flexibility even while holding firm on the policy direction itself. It's not a sign the rules are being watered down; it's a sign of a phased, negotiated rollout. But it also explains why market activity stayed elevated (and even hit record highs) through May and June 2026; the industry had a known runway before the tighter rules actually started biting.

What Changed for Investors

Not every investor is affected the same way by these changes; the impact really depends on how you use leverage, if at all. Here's a breakdown by investor type.

Retail investors using MTF to trade: No direct new restriction applies to you as a trader. But indirectly, brokers now face higher funding costs from the 50% cash collateral rule and the 40% haircut on pledged shares. Expect this to show up as slightly higher MTF interest rates, tighter eligibility on which stocks qualify for margin funding, or both, rather than any outright ban on the facility itself.

Investors taking a loan against shares for personal needs: This is where the rules bite most directly. If your LAS borrowing is well under the new ₹1 crore system-wide cap, day-to-day, nothing changes. But you can no longer route that borrowed money back into buying shares, IPOs, or margin trades; the end-use restriction closes that door specifically.

HNIs and family offices: More exposed than the average investor, since larger LAS/MTF users are the ones most likely to actually hit the new ₹1 crore or ₹25 lakh caps, especially if they were previously spreading borrowing across multiple banks to stay under each lender's individual radar.

Long-term or passive investors not using leverage at all: Minimal direct impact. If anything, you benefit indirectly, a market with more disciplined, better-capitalised leverage is less prone to the kind of sharp, forced-selling shocks that hurt everyone during a downturn, leveraged or not.

| How RBI Rules Impact Different Investors | |||

|---|---|---|---|

| Investor Type | Impact | What Decides It | Our Take for 2026 |

| Retail MTF traders | Low Impact | Whether brokers pass on higher funding costs | Expect modestly higher MTF rates; the facility itself stays available |

| Personal LAS borrowers | Medium Impact | Whether your borrowing nears the Rs 1 crore system-wide cap | Most stay unaffected; large or multi-bank borrowers must adjust |

| HNIs and family offices | High Impact | How much exposure was spread across multiple banks | Real restructuring needed if past the new caps |

| Passive investors | No direct impact | General market stability, not personal leverage | Indirect benefit from a less shock-prone market |

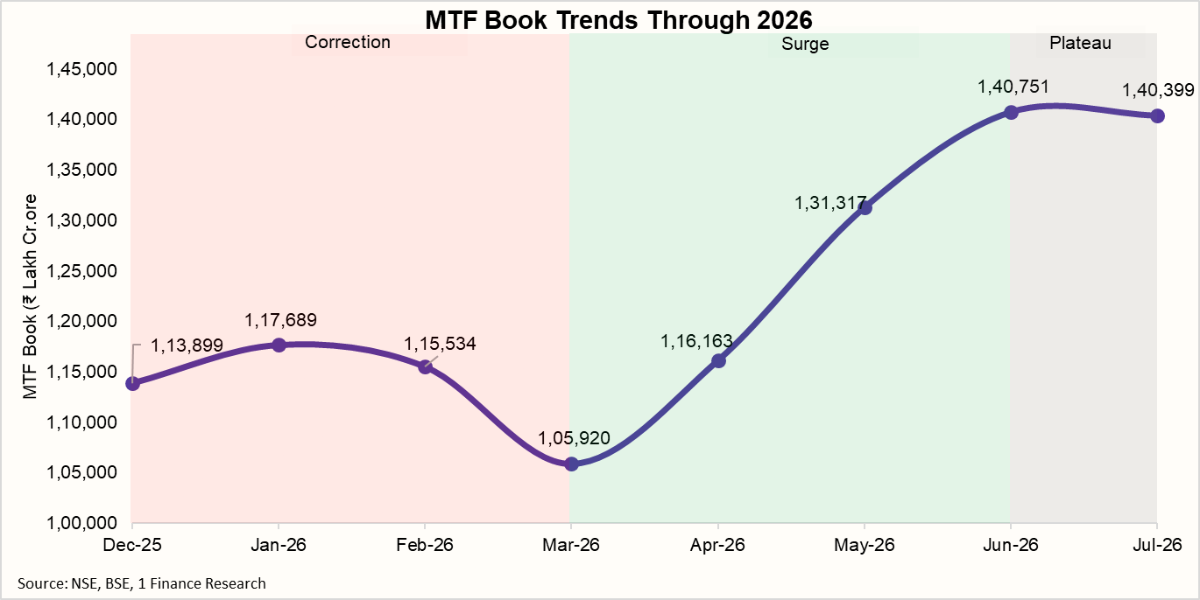

How the Indian MTF Market Moved in 2026

India's combined MTF book (NSE + BSE) had a volatile year, dipping through early 2026 as RBI's new rules loomed, then surging to a record high once the deadline was extended. NSE continues to dominate with roughly 96% of total MTF activity. Interestingly, while RBI tightened funding rules, SEBI has separately explored ways to widen MTF funding avenues for brokers, two regulators pulling in different directions on the same market.

The year broke down into three distinct phases: a correction, a surge, and a plateau.

- Correction phase (Dec 2025 - Mar 2026): rules announced, caution sets in, book falls 14%

- Recovery/surge phase (Apr - Jun 2026): deadline extended, book jumps 33% to a record

- Plateau phase (Jul 2026): extended deadline kicks in, growth flattens

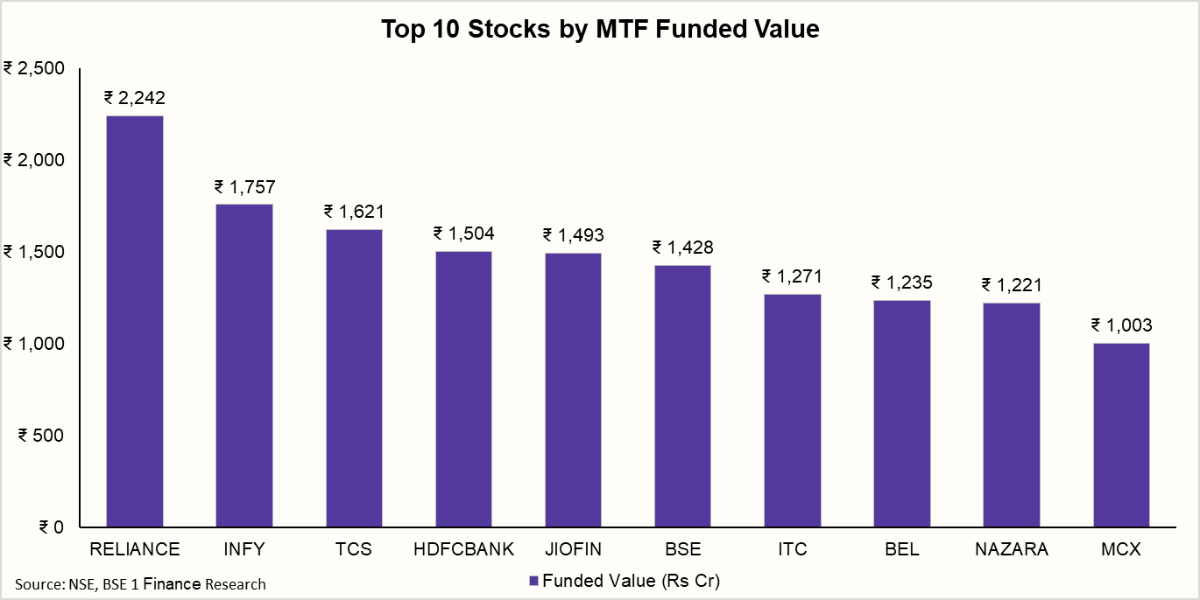

Which Stocks Have the Highest MTF Exposure

Looking at which specific stocks investors are leveraging shows where conviction and risk are concentrated. As of July 7, 2026, the picture looks like this:

Top stocks by combined funded value (NSE + BSE): Reliance Industries leads by a wide margin, with a combined funded value of ₹2,242 crore, well ahead of Infosys (₹1,757 crore) and TCS (₹1,621 crore). HDFC Bank and Jio Financial Services round out the top five at ₹1,504 crore and ₹1,493 crore, respectively. The list is dominated by large, liquid names, Reliance, the IT majors, HDFC Bank, which is typical of MTF activity, since brokers and risk systems favour highly liquid, lower-volatility stocks for leveraged exposure.

Where fresh leverage is building: On a day-on-day basis, Trent led funding increases with ₹193 crore added, followed by HSCL (+₹94 crore) and L&T (+₹79 crore), pointing to leveraged interest building in retail and infrastructure names, alongside continued appetite for Reliance itself (+₹38 crore).

Where investors are pulling back: Infosys saw the sharpest funding decrease, down ₹127 crore in a single day, followed by Persistent Systems (−₹62 crore) and Swiggy (−₹55 crore). Notably, IT stocks dominate the decrease list (Infosys, HCLTech, TCS, TechM all appear), suggesting some cooling of leveraged conviction in the sector even as it remains among the top-funded overall.

Why this matters: This granularity is genuinely useful for advisors: leverage is concentrated in blue-chip, liquid names (lower single-stock risk), but day-to-day flows show real-time shifts in sentiment, IT stocks are seeing funding pulled out even as retail/infra names see fresh leveraged buying.

What Advisors and Investors Should Know About MTF Risk

Leverage magnifies both gains and losses, and historically, a large majority of retail traders using leveraged products in India have ended up on the losing side. MTF doesn't change those odds; it just changes the size of the outcome. There's also a structural risk worth flagging: Zerodha founder Nithin Kamath has publicly warned that a sharp market fall could trigger many brokers' risk systems liquidating leveraged positions at the same time, deepening the fall further, a risk that exists at the investor level regardless of what RBI's bank-side rules do.

Practical talking points for client conversations:

- Set a personal leverage cap, and stick to it regardless of how confident a position feels

- Maintain strict stop-loss discipline, especially in volatile months (March 2026's correction is a useful real-world reference)

- Avoid concentrating leveraged exposure in a single stock or sector

- Treat MTF interest as a real, compounding cost, not a minor detail; it adds up quickly over longer holding periods

With the MTF book at a record high and RBI's tighter rules only just taking effect from July 1, this is a genuinely good moment for advisors to proactively check in with clients using leverage, before market conditions test it, not after.

What to Expect Next

2026 has been a tug-of-war between rising retail appetite for leverage and regulators trying to rein it in. The MTF book fell to ₹1.06 lakh crore in March, then surged to a record ₹1.40 lakh crore by July, even as the RBI tightened LAS rules and forced brokers into costlier, more disciplined bank funding.

Near-term: Expect leverage growth to moderate, not collapse. July's numbers already show the book essentially flat, an early sign that the tighter rules may be starting to bite. Investors should expect slightly higher MTF rates and more selective margin eligibility.

Medium-term: Brokers reliant on bank credit face a real competitive disadvantage against self-funded players. Meanwhile, RBI and SEBI are pulling in different directions, RBI tightening bank-backed leverage, SEBI exploring ways to widen broker funding access, a tension worth watching.

Bottom line: RBI isn't trying to kill leverage in Indian markets, it's trying to make sure it's built on sturdier foundations. For investors and advisors, the takeaway is simple: use leverage deliberately, understand its real cost, and don't assume today's record numbers are permanent.