For months, the government maintained that the Strait of Hormuz crisis was manageable. Fuel prices stayed frozen. Gold imports flowed freely. The message to markets was: we've got this. Then, in the span of one week, everything changed. The Prime Minister urged the nation to carpool and skip gold purchases. Import duties on bullion were doubled overnight. And fuel prices, untouched for 49 months, finally moved. These are not the actions of a government that has things under control. These are the actions of a government that has decided the cost of pretending is now higher than the cost of acting. The question for advisors is straightforward: how far does this adjustment go, and what breaks along the way?

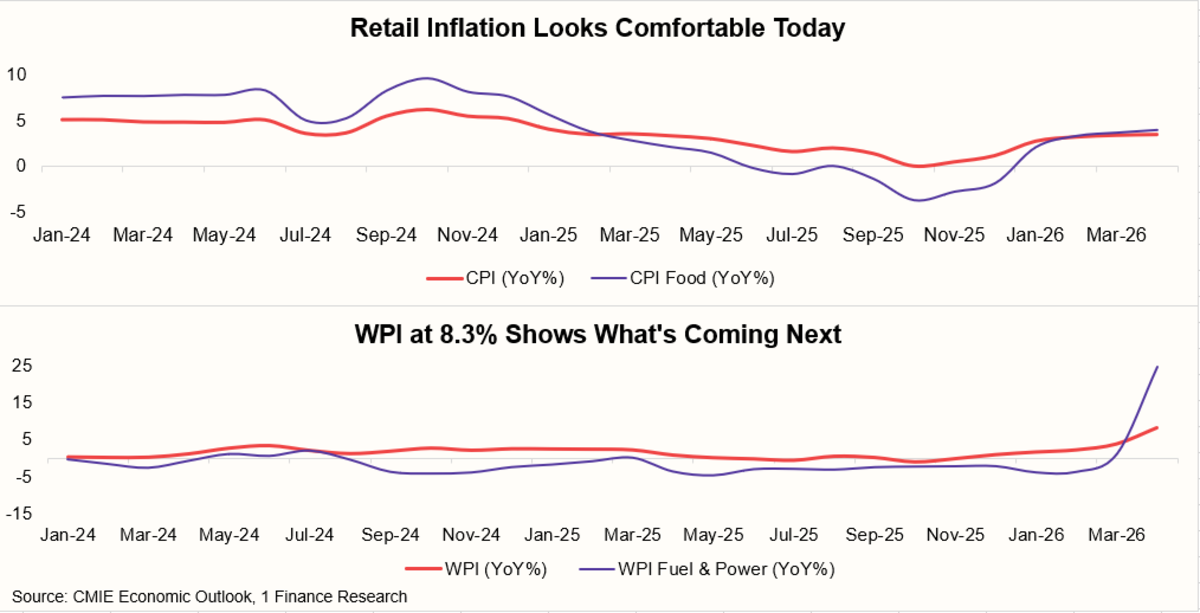

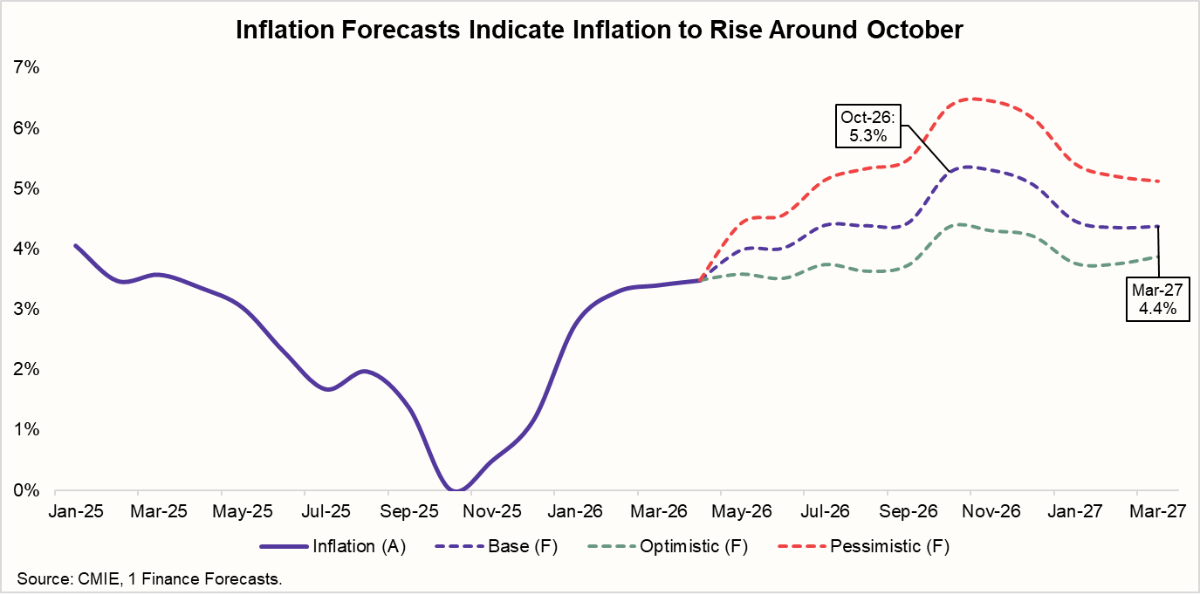

CPI Is Still Comfortable, but Wholesale Prices Are Screaming

April's CPI print came in at 3.48%, up marginally from 3.40% in March and well inside the RBI's 2-6% tolerance band. Food inflation ticked up to 4.20% from 3.87%, driven by tomatoes (+35.3%), cauliflower (+25.6%), and food services.

And those wholesale costs have exploded. WPI inflation surged to 8.3% in April from 3.88% in March, a 42-month high. The fuel and power component hit 24.71%, up from just 1.05% the previous month. Crude petroleum WPI inflation printed at 88.06%. Petrol at 32.4%. Diesel at 25.2%. Primary articles rose 9.17%. Manufacturing costs accelerated across basic metals (+7.0%), chemicals (+5.1%), and textiles (+4.9%). On a month-on-month basis, the WPI jumped 3.86% in April alone.

💡WPI has historically led CPI by two to three months. When wholesale prices surge, the pressure flows downstream through freight rates, farm input costs, and manufacturing margins before showing up on retail shelves. In April, WPI outpaced CPI by 4.8 percentage points, the widest since mid-2022. |

The new CPI series, which updated basket weights based on the latest Household Consumption Expenditure Survey, actually increased the share of non-food items, including transport. That means the fuel hike will register more prominently in headline inflation than it would have under the old series. We expect CPI to breach 5% by Oct if crude stays above $100/bbl.

Compounding the pressure: IMD has forecast below-normal monsoon rainfall at 92% of the long-period average, with a 35% probability of a deficient season. El Niño conditions are expected to develop by the second half of the monsoon, potentially suppressing rainfall across Rajasthan, Punjab, Haryana, and the core rainfed regions of central and western India. A weak kharif season would push food inflation higher precisely when fuel pass-through is hitting CPI.

Rs 3 Per Litre Barely Scratches the Surface

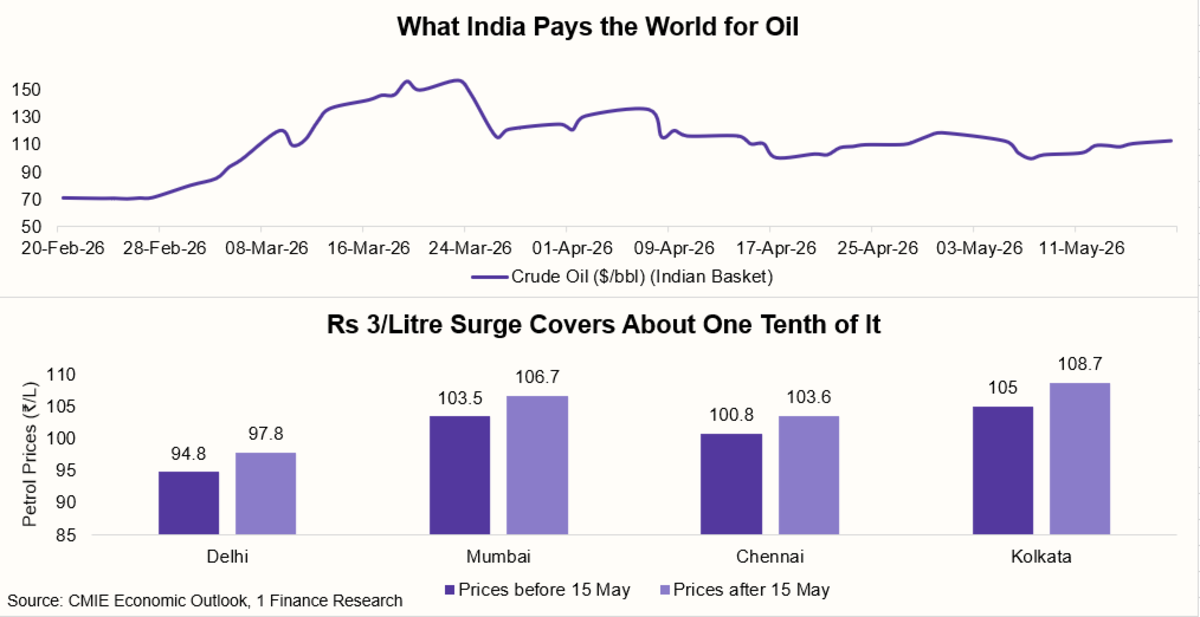

The fuel price hike announced on May 15 ended a 49-month freeze, the longest since deregulation began. Petrol now costs Rs 97.8/litre in Delhi and Rs 106.7/litre in Mumbai.

But the real number to watch is not Rs 3. It is Rs 25 to Rs 28.

That is the correction required to bring retail prices closer to current crude-linked economics. The gap is massive. India’s crude import basket averaged around $69 per barrel before the shock and moved into the $113–114 range in April. That is a 64% surge. OMCs were reportedly losing around Rs 100/litre on diesel and Rs 20/litre on petrol before this hike. A Rs 3 correction covers roughly one-tenth of the gap.

That leaves three possibilities. More hikes may follow in stages. The government may absorb part of the burden through excise adjustments, which would pressure the fiscal position. Or oil marketing companies may continue to carry large under-recoveries. None of these outcomes is painless.

The External Account Is Under Real Pressure

The fuel hike and the policy scramble that followed make more sense when you look at what happened to India's trade account in April. The merchandise trade deficit widened to $28.4 billion, a record for the month and $8 billion wider than March. Imports surged 10% YoY to $71.9 billion, the highest ever for an April, driven almost entirely by crude oil repricing. Exports rose a healthy 13.8% to $43.6 billion, but cannot grow fast enough to offset an import bill that is structurally inelastic to price.

The FY26 full-year picture frames the vulnerability clearly:

Metric | FY25 | FY26 | Change |

|---|---|---|---|

| Total exports (goods + services) | $825.3 bn | $860.1 bn | +4.2% |

| Total imports (goods + services) | $919.9 bn | ~$979.4 bn | +6.5% |

| Merchandise trade deficit | $283.5 bn | $333.2 bn | +17.5% |

| Overall trade deficit | $94.7 bn | $119.3 bn | +26.0% |

| Gold imports (value) | $58.0 bn | $72.0 bn | +24.1% |

| Gold imports (volume) | 757 tonnes | 721 tonnes | -4.8% |

| Services trade surplus | $188.8 bn | $213.6 bn | +13.1% |

Two things stand out. First, the merchandise deficit widened by nearly $50 billion in FY26, despite crude oil import costs easing in some parts of the year. The main culprits were gold imports, which rose to a record $71.98 billion even as volumes fell, and electronics imports, which climbed 16.2% to $119 billion.

Second, services exports of about $418 billion continued to provide a crucial buffer, helping contain the overall trade deficit even as the merchandise gap expanded sharply.

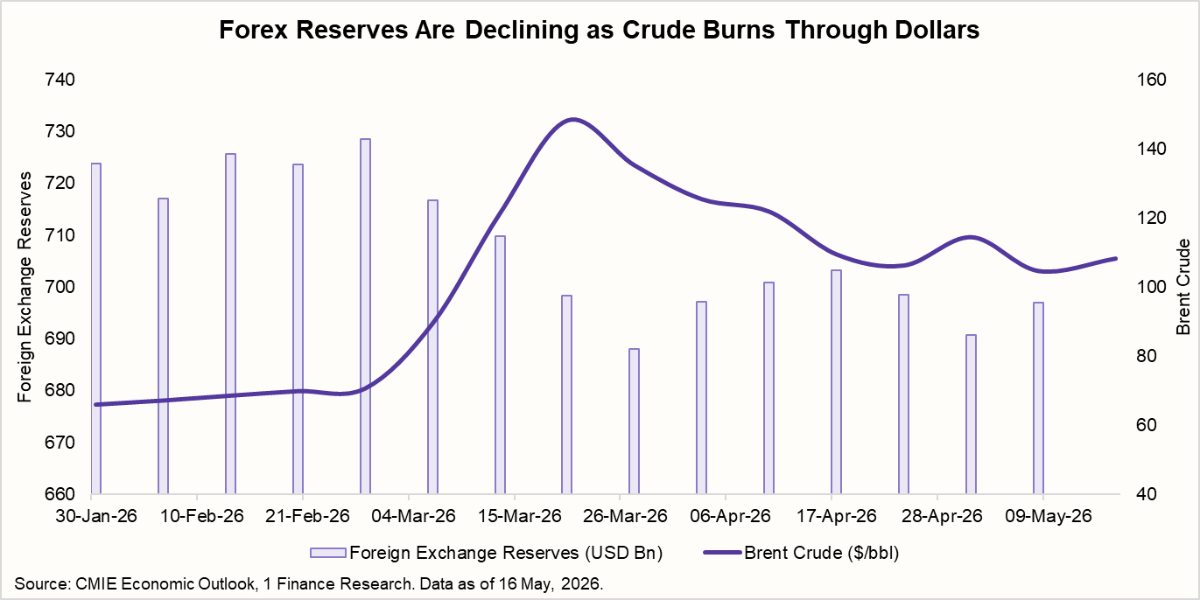

The current account deficit was a comfortable 1.3% of GDP as of Q3FY26. That number is already history. With crude above $100/bbl, CAD is projected above 2% of GDP for FY27. Every $10/bbl increase in crude adds roughly 40-50 bps to the deficit. At $110 Brent, we are looking at an additional $25-30 billion on the annual oil import bill compared to FY26 averages.

On the forex side, reserves stood at $697 billion as of May 8, recovering slightly from $690 billion the previous week but down roughly $38 billion since the war started in late February. Reserves have been drawn down as the RBI has intervened to smooth the rupee’s decline and cushion the external shock. Import cover sits at roughly 9 months. The rupee, at 96.3 (as of May 19) per dollar, has depreciated 12.6% over the past 12 months, making it Asia's worst-performing major currency in 2026.

| 💡Did you know? India spent $174.9 billion on crude and petroleum products in FY26, or 22% of its total imports. Add gold at $72 billion, and these two commodities alone account for over a third of India's entire import bill. |

This is the backdrop against which every policy action of the past week needs to be read.

Gold Duties Are a Forex Tool, Not Just a Tax Move

On May 10, the Prime Minister addressed a rally in Hyderabad and made four specific appeals: reduce fuel consumption, avoid buying gold for a year, cut unnecessary foreign travel, and adopt electric vehicles. Three days later, the government raised gold import duties from 6% to 15%.

Here’s what it changes:

Component | Earlier | Now |

|---|---|---|

| Basic Customs Duty | 5% | 10% |

| Agriculture Infrastructure Development Cess | 1% | 5% |

| Effective Import Duty | 6% | 15% |

Including IGST, the total levy on bullion is now 18.45%, up from 9.18%. Here's what that means in rupee terms for 10 grams of gold at the current international price of Rs 1,58,347:

Scenario | Duty Rate | Duty Amount (on ₹1,58,347) | Landed Value After Duty |

|---|---|---|---|

| Earlier structure | 6% | ₹9,501 | ₹1,67,848 |

| New structure | 15% | ₹23,752 | ₹1,82,099 |

This is not a revenue play. Average monthly gold imports rose to 83 tonnes in early 2026 from 53 tonnes in 2025, despite prices climbing. Gold is a non-essential import from a macroeconomic standpoint, but reducing demand is notoriously difficult in India, where bullion serves as savings, collateral, and cultural tradition simultaneously. The duty hike is the fastest lever available to compress the import bill. Early signs suggest it is working: traders have paused imports, and physical demand is shifting toward the secondary market and recycled gold.

The risk, as always with high gold duties, is smuggling. The government cut duties sharply from 15% to 6% in 2024 precisely to curb illegal imports. Reversing that cut within two years signals how urgently the external balance needs protection right now.

The UAE Deal Is a Genuine Positive

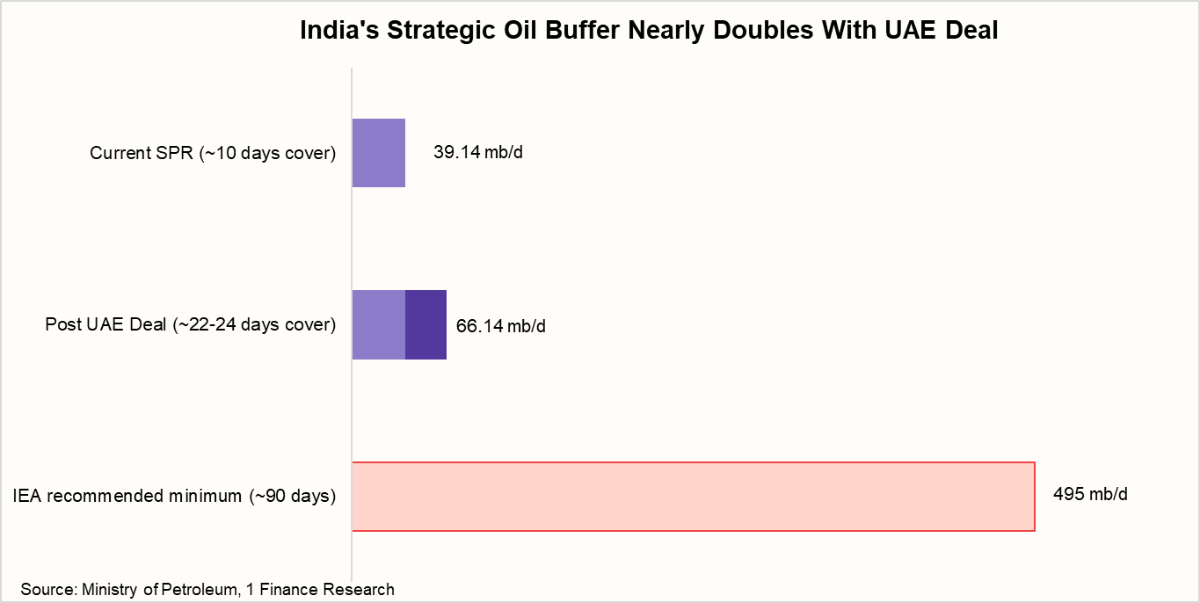

Amid the defensive measures, one development was genuinely constructive. On May 15, during PM Modi's visit to Abu Dhabi, India and the UAE signed an agreement for ADNOC to store up to 30 million barrels of crude oil in India's Strategic Petroleum Reserve. The deal also includes the establishment of strategic gas reserves in India and long-term LPG offtake supply agreements. Separately, the UAE committed $5 billion in new investments.

India's existing SPR across Visakhapatnam, Mangaluru, and Padur holds roughly 39.14 million barrels, about 10 days of consumption. Adding 30 million barrels could extend emergency cover to 22-24 days. The Fujairah storage component adds geographic diversification; oil stored in the UAE reaches Indian ports faster than distant alternatives. In a supply disruption, logistics speed matters as much as volume.

That said, three caveats are worth noting.

- First, the 30 million barrels are aspirational, not immediate. The Chandikhol facility in Odisha doesn't exist yet, and Visakhapatnam needs expansion, this takes over years, not months.

- Second, the Fujairah storage component, while it creates geographic diversification, is not risk-free. Fujairah was itself targeted by Iranian strikes earlier in the conflict, and storing India's strategic reserves in an active conflict zone doesn't eliminate geopolitical risk.

- Third, UAE's own crude production fell to 2.02 million b/d during the Hormuz disruption versus its 3.4 million b/d capacity, raising questions about its ability to fill India's reserves during the very crises when they'd be most needed.

We view this as the most significant SPR development since the programme's inception. It doesn't solve the immediate supply squeeze, but it materially improves India's structural resilience.

What to Expect From the June MPC

The RBI MPC meets June 3-5. In April, the committee voted unanimously to hold at 5.25% with a neutral stance. Since then: fuel hike announced, gold duties raised, Brent past $108, rupee past 96, monsoon forecast below normal, WPI at a 42-month high, and FPIs fleeing at record pace.

Our base case: hold at 5.25% with language shifting toward acknowledging upside inflation risks. A cut is unlikely; the rupee cannot afford a wider rate differential with the US while capital is already exiting.

If June and July CPI prints confirm the upward trajectory, an explicit hawkish tilt by August becomes likely. For rate-sensitive sectors, the implication is clear: the easing cycle that delivered 125 bps of cuts in 2025 is over.

What Advisors Should Watch Next

The next few weeks will tell us whether these are isolated adjustments or the beginning of a broader policy reset.

- Watch CPI over the next few weeks for fuel pass-through into food, transport, and logistics.

- Track the rupee closely, since further weakness would add pressure to inflation and reserves.

- Monitor crude prices, especially if Brent stays above $100 per barrel.

Advisors should also watch the monthly gold import data. If the duty hike works, import volumes should slow. If they don’t, the government may need to tighten further. The same logic applies to fuel. If under-recoveries remain large, either retail prices must rise again, or the fiscal cost must be absorbed elsewhere.

Sector-wise, oil marketing companies remain under pressure, consumer businesses face margin risk, and import-heavy sectors are vulnerable to currency weakness. Exporters benefit from the weaker rupee, but they may still face a global demand slowdown if higher oil prices hit growth worldwide.

The Real Message

The government has not magically solved the oil shock. It has simply stopped pretending that it could avoid adjustment forever.

That is an important shift. It means India is now moving from reassurance to response. The fuel hike, gold duty increase, PM’s appeal to conserve, and the UAE reserve deal all point in the same direction: the external shock is real, and the policy response has begun.

The question now is not whether India will adjust. It already has. The question is whether these are the first steps of a controlled recalibration or the early stages of a much bigger macro stress cycle.